Have you noticed how few senior citizens are eating dog food these days?

Apparently Rick Perry hasn't.

Instead, in a kind of right-wing reflexology, he decided to blurt out, in last night's GOP candidate's debate, that Social Security is a "Ponzi scheme."

It is?

Actually, it isn't.

I know a little bit about Ponzi schemes as I was involved a little on the periphery of the Bernie Madoff Ponzi scheme fraud investigations. You can read a bit about that here or check out the movie (Chasing Madoff) which is playing in theatres now.

I know quite a bit about Social Security too. Social Security is not a Ponzi scheme; It's a progressive, inter-generational retirement insurance system and it is, to be clear, one of the best funded retirement insurance systems in the world.

Read that last statement again.

Social Security is almost certainly better funded and more robust than any defined benefit retirement system you have ever paid into, and it is almost certainly doing better than your 401K defined contribution plan which has, no doubt, taken a massive bullet in the head thanks to the failed economic policies of the last Texas Governor we elected to the Oval Office.

34343434

By way of background, let me say that back in the Clinton era, I spent eight years defending Medicare and Social Security from attack, initiating the conversation (still ongoing) about drug reimportation from overseas, and trying to derail misguided efforts to privatize Social Security.

I bring this up not to rehash the past but because since then a lot has happened, including the collapse of the financial markets under the George W. Bush Administration, the collapse of the housing market under the George W. Bush Administration, and the wholesale shedding of U.S. jobs, which began under the George W. Bush Administration.

What does any of that have to do with Social Security?

Actually, quite a lot.

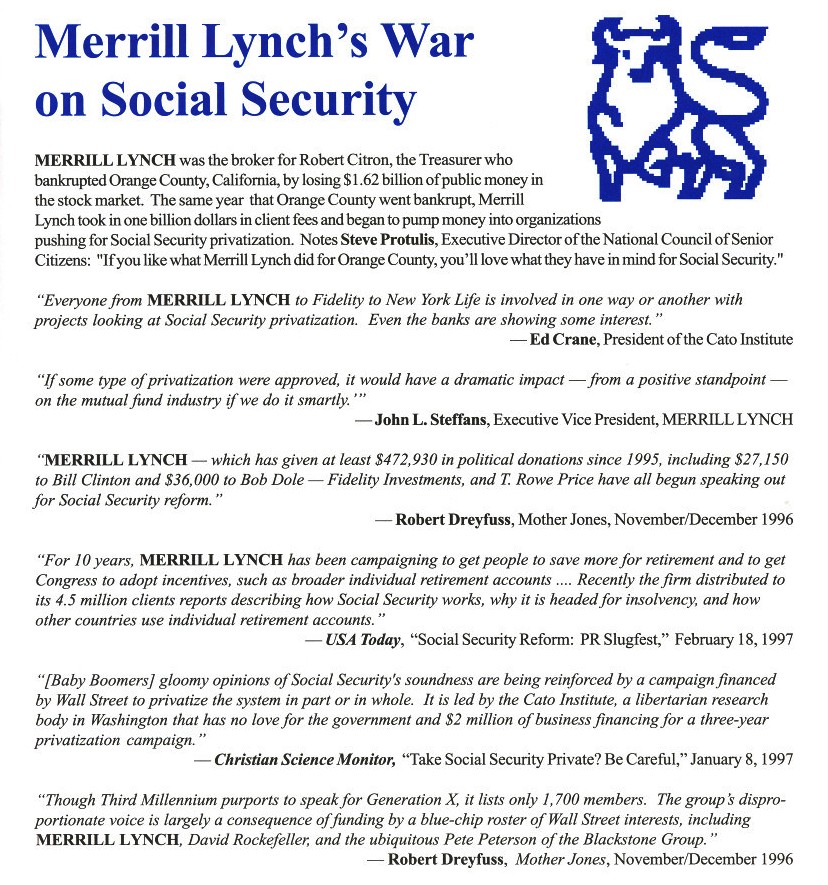

You see, back in 1996, the folks who were pushing to privatize Social Security were Wall Street firms like Merrill Lynch, Morgan Stanley, and Goldman Sachs.

Brokerage houses were salivating at the prospect of skimming off hundreds of millions of dollars a year in commissions and transaction fees from a privatized system.

All that had to occur for that to happen, was to sing the siren song of greed.

And, of course, the stage was well set. Back in the mid-1990s, everyone from cab drivers to fresh-scrubbed college grads were convinced they were stock-picking geniuses. The market was roaring! Surely any fool could make a mint on Wall Street? It was simply a matter of tossing a dart, and never mind if anyone said differently!

Wall Street knew an opportunity when it saw one, and so it pumped hundreds of millions of dollars into a campaign designed to leverage fear, resentment, and greed into a new profit center for the hyper-rich.

{kind=link}

The fear being fanned was the notion that Social Security was "going to go broke." And never mind that it was not true.

The resentment being fanned was the notion that someone, somewhere, might be getting something they did not quite deserve.

The big emotional driver, of course, was greed.

Think about how much money you could be making if you invested in such sure-fire winners as Hewlett-Packard or Pets.com or Tenet Healthcare!

What could go wrong? Nothing! Stocks were soaring!

Of course, to buy the cure you first had to buy the disease.

Social Security was terribly sick said Wall Street.

The cause of the disease, said the stock market sages, was that America was aging.

We were going to go broke because we were growing old.

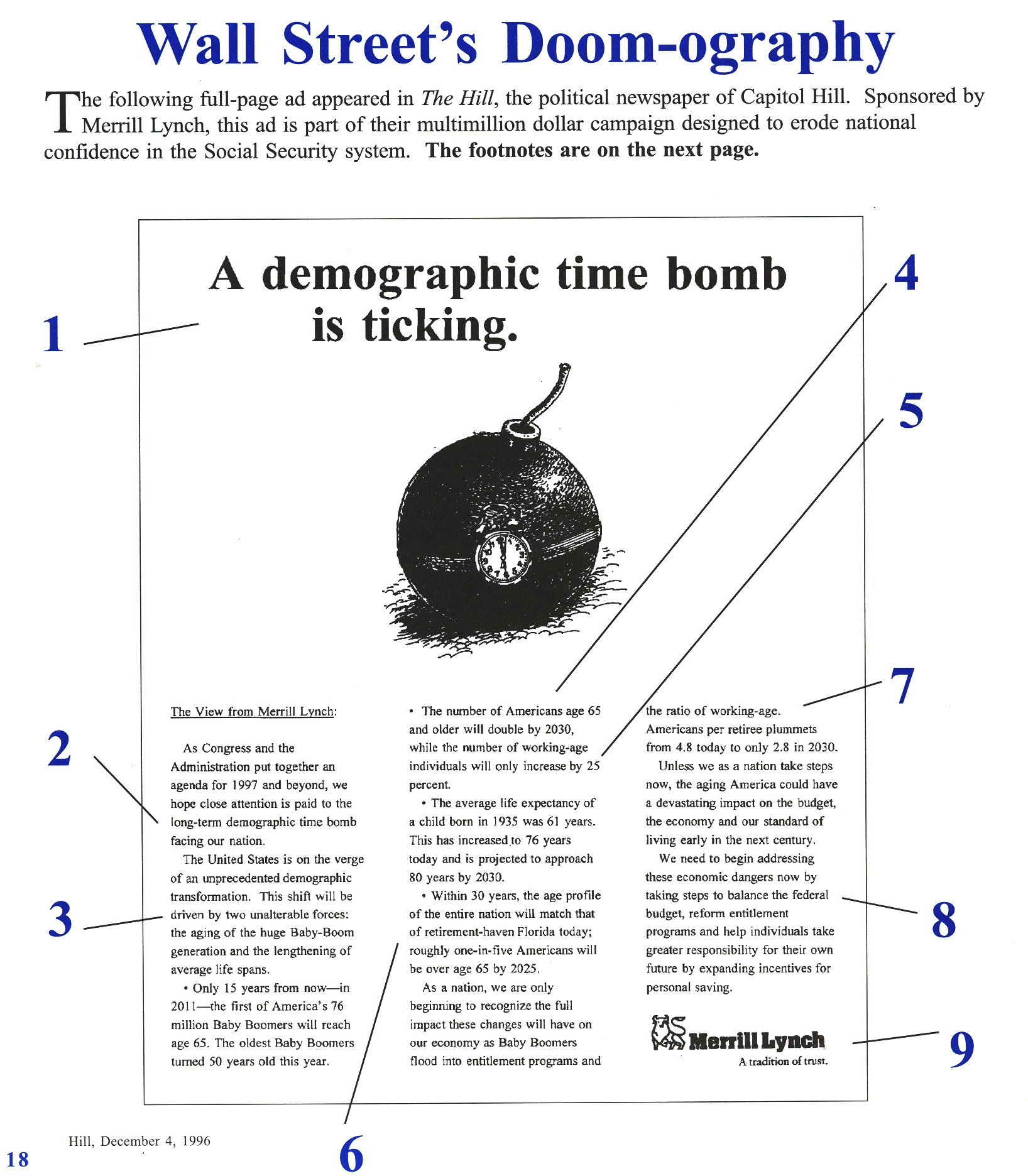

And so Merrill Lynch and other brokerage firms ran full page ads, such as the one below, talking about the demographic "time bomb" of Social Security.

.

.

Click on the ad, above, to read the full text. And click here to read the annotations, numbered in blue, to read how Merrill Lynch was trying to fear-monger us into killing Social Security.

{kind=link}

Of course it was all nonsense, but it was potentially lucrative nonsense for Wall Street traders, and so it was asserted, repeated, parroted and echoed across the landscape by folks who overtly or covertly were taking vast sums of money from Wall Street.

Not everyone was on the take, of course. A lot of people were simply ignorant.

The ignorant did not know the benefits of an aging population, nor did they understand the liabilities of a rapidly growing one.

Casual pundits did not know the difference between one kind of dependency ratio and another.

And Wall Street knew that.

They sought to tell a simple story, no matter if it was a lie.

It was enough if it sounded true. Greed, fear and resentment would do the rest.

We were told "Social Security was like the Titanic."

Which was true, except that we were 30 miles from the iceberg, we were sailing on a clear day, and we had an attentive watchman on deck. If we made a quarter of a degree change in course, we would sail so far from the iceberg we would never know it was there.

But Wall Street traders wanted us to panic. They wanted us to sink the boat NOW in order to avoid hitting the iceberg 30, 40 or 60 years into the future.

Now, it's true that if you sink the boat, you will not hit the iceberg. But that's cold comfort when you're treading water, alone, in the North Atlantic.

The good news is that through sheer force of fact, rhetoric and some luck, those of us working to derail Wall Street privatization efforts manged to stall things long enough that the stock market had a major "correction."

Which is a nice way of saying that a few million people who thought they were geniuses, lost their shirts and learned a fundamental mathematical fact: If you lose 50% of your portfolio's assets during a "correction," it takes 100% growth in that same portfolio just to be made whole again.

A small lesson was learned. But it was a small lesson, and not everyone learned it. And, truth be told, we are a nation of amnesiacs. We have rafts of politicians who are slow learners and quick forgetters.

And Wall Street is nothing if not patient.

And behind it all, always just out of sight, remain the discrete men and women with bags of cash who are only too eager to lubricate the wheels of Capitol Hill.

They are people like the professional Wall Street lobbyists surrounding Rick Perry.

And so, because we still have Wall Street rats in the grain pile, we still have folks like Rick Perry staggering up to podiums to talk about Social Security as a "Ponzi scheme" whose solution is privatization.

A politician expressing dismay that Social Security is a multi-generational transfer program is a bit like a a mechanic saying he is terrified that explosions occur inside a gasoline engine; it is a statement that does not inspire confidence in the repair job being suggested. Does this Bozo even know how the system works??

And, of course, the answer is NO.

Nor does Rick Perry know the first thing about demographics. Demographic change is not going to bankrupt this nation. And I guess I would know: I am a demographer who has spent a lot of time with the Social Security actuarial and economic-variable tables.

Social Security is sound now, and it will be sound into the future.

But you know what is not sound?

Merill Lynch.

Goldman Sachs.

Lehman Brothers.

Morgan Stanley.

All of these Wall Street firms are gone, bankrupted, restructured, or boned out to foreign investors.

These companies once wanted to run your life, but in the end it turned out they were all liars, cheats and thieves whose own house of cards came tumbling down around them.

Now Rick Perry is peddling the latest version of Wall Street's Koolaid.

No problem. Vote for who you want to.

That said, remember this: If you are prepared to drink Wall Street's Koolaid, you must also be prepared to eat their dog food.

So if Rick Perry sounds good to you, put away the Lean Cuisine, and open up a can of Alpo and plop it down onto a plate and take a good long look.

That has been Wall Street's solution in the past. This was Wall Street's solution in 1929. And this is what they're offering us today; the left overs bits, cut away and rendered after they take the choicest cuts for themselves.

Welcome to the Dog Food Economics of Rick Perry! Now eat up!

- Related Post:

** Cancer and Chemo

** The Candidate Was "Pre-Vet"?

** You Call That a Watchdog?

** Ratting in America's Economic Barn

6 comments:

Thank you for another clear and compelling post. It occurred to me that Wall Street has something in common with The Taliban. They both are deadly patient.

Seahorse

Wall Street has done far more damage to America that the Taliban or Al Queda. One destroyed two buildings and 3,000 lives, the other destroyed our entire economy and ruined 30 million lives. If we were serious and really lauched a war on fraud, Seal Team Six would be dropping out of helicopters into corporate board rooms every night.

P

Great post. Bush 2 did incalculable harm to this nation. The question now is whether Obama will go down for it, since even Jesus would struggle with the hand Obama was dealt and the economy still stinks. If the voters demand a miracle, you are right: they may be eating dog food.

Agreed entirely about the relative quantity of damage inflicted. I guess my point is that out-waiting their opponents, or perhaps in Wall Street's case, their quarry, is a simple method to their success.

Seahorse

OK, I'll bite. So, we've been told for enough years that Social Security is running out of money and will not have enough money to pay its obligations when I retire. (I'm not quite 30.)

So, aside from your insistence that it's well funded, what 'facts' are being quoted by the fear mongers, and why are those the wrong facts, what are the right facts, and most importantly. When I want to retire in 35-40 years, am I going to receive Social Security payments, or should I just consider my Social Security payments as a way of repaying my parents for rearing me?

Also, since you're the one with expertise, what do you think of the 2% payroll tax break we're currently enjoying, and what about the 4.2% additional break the President would like to pass?

Also, as a worker, do I get to be upset that my Social Security is now being 50% funded, so I should be saving that money myself, but 3/4 of the latest tax break is going to my employer, so if I want to save the same as earlier, I need to save 4.2% of my income next year, while only receiving a 1.1% tax break?

Just curious, thanks as always for the thought provoking posts.

You might want to start by reading the footnotes in that graphic I embedded (links to footnote embedded in text).

The short story is that there are a LOT of numbers that go into Social Security's long term actuarial projections and the bias is to put ALL the numbers towards the worse case scenario, which the experts know is WRONG, but still good longer-term planning as no one will ever complain if there is extra money in the "till" in 2050.

So what are the numbers? A smattering: population growth, productivity, lifespan, work span, labor force paricipationr rates, and wages (just for starts).

To begin with, the Census Bureau's mid-range projections are ALWAYS too low (I have written about that on here before), while their productivity numbers are also not too good as they are having a hard time keeping up with technology.

For two links on that see: http://unbiasedopinion.blogspot.com/2011/09/demographcs-vs-doomographics.html (put that up today just for you), and also this cenus bureau link which shows you the population variance between high and low from 2000 to 2050 > http://www.census.gov/population/www/pop-profile/natproj.html

You will note that the 50 year population variance alone is 100 percent between the low and the high! The same skew exists in the other data. Go back 30 years and think of what we could not have imagined in terms of productivity, spending, wages, labor force, immigration... the same will be true 30 years into the future.

That said, even under the worse case scenarios, Social Security NEVER "goes broke." If everything goes as bad as it possibly could and NOTHING changes up to the moment of impact (we know that's not happening), then Social Security still pays out 75 percent. See >> http://www.msnbc.msn.com/id/7080681/ns/business-answer_desk/t/social-security-really-going-broke/

For purposes of comparison to the private market, if you have a defined benefit pension and your company goes broker, the Pension Benefit Guaranty Corporation (PBGC) will only pay 75%. Of course, most folks don't have defined-benefit pensions now, they have 401K, and they are: 1) not paying into them; 2) not paying enough into them or starting too late; 3) robbing their 401Ks while unemployed in bad times or for luxuries during good times, or; 4) investing in stocks which have tanked (the average 401K balance fell 27% in 2008).

Let me tell you a single Social Security fix and how small it is, and how much it fixes.... Simply eliminating the Social Security payroll tax so that people with incomes of over $106,000 a year pay Social Security taxes on all income over that number. That single reform would eliminate about 90% of the Social Security shortfall! This is what I call the "secret of the gilded class." Most folks DO NOT KNOW that rich people stop paying Social Security taxes on income over a certain amount. No other tax does this, not even Medicare! And, of course, it's ridiculous that members of Congress stop paying SS taxes around the Fourth of July, while the folks who scrub the halls in that building are paying 365 days a year.

Other obvious reforms are needed, but will have no impact on the U.S. population. For example, we can stop paying Social Security benefits to illegal aliens and resident aliens. And why not? These folks aren't American citizen. Illegal aliens broke our law and permanent resident aliens who choose to not become citizens can also choose not to get Social Security. We owe things to citizens, not non-citizens.

I could do policy stuff like this all day long... but why? Social Security is taking in far more money than it is spending right now and it is not getting more broke, it is getting less broke. Ditto for Medicare, by the way.

P

Post a Comment